0

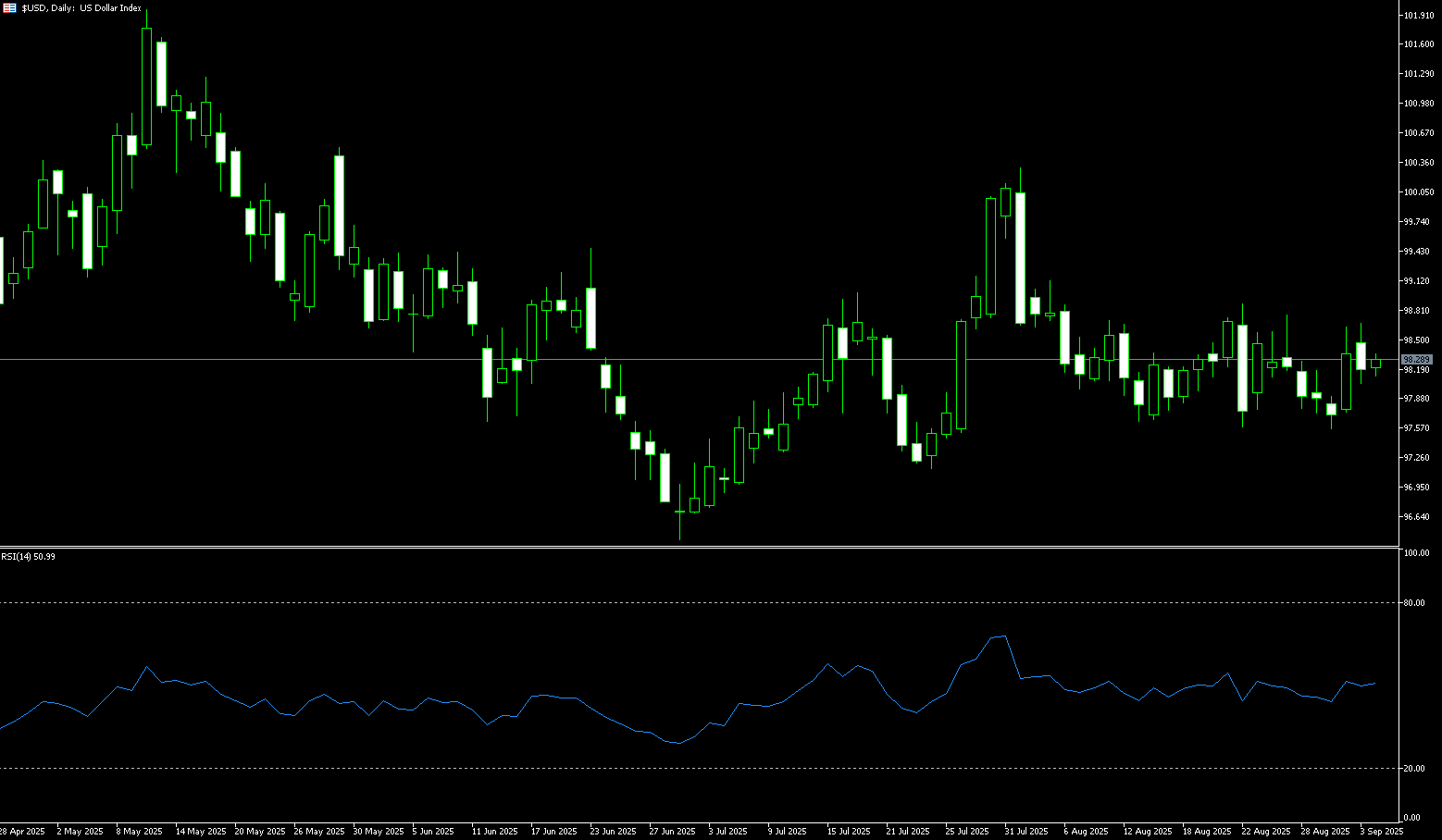

US Dollar Index

The US dollar index fell below 97.50 on Monday, snapping a three-day rally. Traders are awaiting speeches from several Federal Reserve officials this week for clues on the policy outlook. St. Louis Fed President Alberto Musallem said interest rates are currently "between moderately tight and neutral," and he sees limited room for further cuts without becoming overly accommodative. Last week, the Fed cut its first interest rate this year and hinted at another 50 basis point cut, although Chairman Powell emphasized that the move does not mark the beginning of a new easing cycle. Focus also shifted to Friday's PCE report for fresh insights into inflation trends. The US dollar weakened primarily against the euro, Canadian dollar, and British pound, while remaining stable against the Japanese yen and Swiss franc. Traders will closely monitor speeches from Fed officials later this week, as they could influence currency markets. Concerns about the Fed's independence could limit the dollar's upside.

The US dollar index's rebound continues, with short-term focus on the resistance range of 98.08 (50-day simple moving average) to 98.11 (September 11 high). The 14-day Relative Strength Index (RSI) on the daily chart has risen to around 49.50, indicating a neutral to positive range. If the US dollar index successfully breaks through the 08.08-98.11 range, the next target will be 98.46 (100-day simple moving average). If resistance is encountered in this range, renewed selling pressure could be triggered towards 97.20 (5-day simple moving average) and the 97.00 (round number mark). A decisive breakthrough would reinforce bearish sentiment towards 96.38 (previous low).

Consider shorting the US Dollar Index at 97.45 today, with a stop-loss at 97.58 and targets at 97.00 and 96.90.

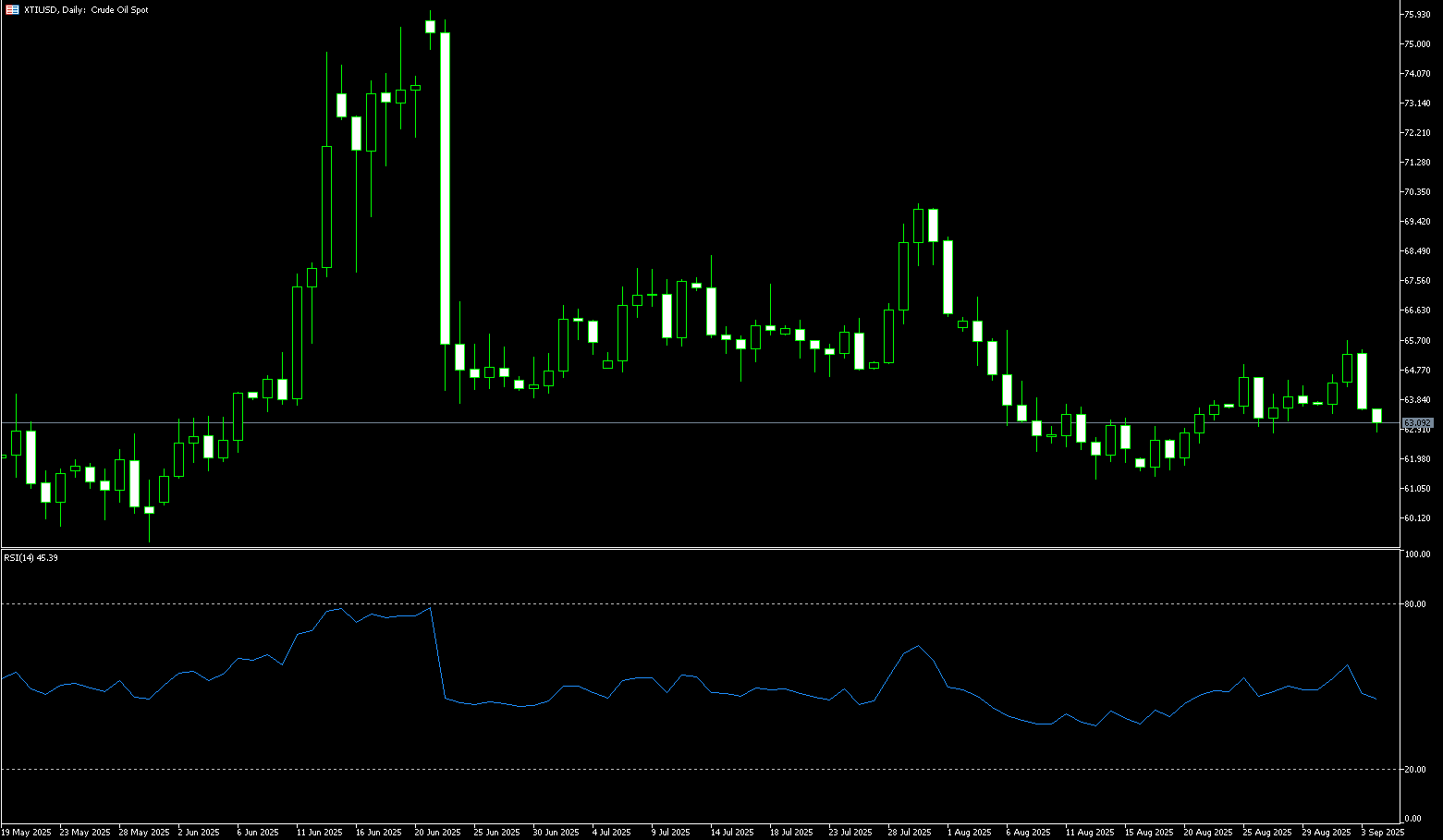

WTI Spot Crude Oil

WTI crude oil retreated to around $62.20 per barrel on Monday after three consecutive days of decline due to the possibility of additional EU sanctions against Russia. The EU proposed its 19th round of sanctions against Russia on Friday, aimed at pressuring Moscow to end the war in Ukraine. The plan includes a ban on Russian liquefied natural gas imports into the EU starting January 1, 2027, as well as sanctions on 118 additional shadow vessels and Chinese and other foreign companies involved in purchasing Russian oil. However, oil price gains are limited by concerns about ample supply and ongoing weak demand. Iraq has reportedly increased its oil exports, adding to supply pressures amid the gradual easing of voluntary production cuts under the OPEC+ agreement.

If oil prices rebound this week, it will likely come from short-term geopolitical risks, but their sustainability is questionable. Crude oil is generally consolidating, but its bearish bias remains. The 14-day Relative Strength Index (RSI) remains below the neutral 50 level, and prices remain within a three-year descending channel extending from the 2022 high. However, in the short term, if oil prices can clearly hold above $64, bullish momentum could propel prices to retest the yearly high and challenge the upper boundary of the three-year descending channel. On the upside, a break above $64.00 (a psychological market barrier) and the 100-day simple moving average (SMA) at $64.37 could target $65.61 (the 50.0% Fibonacci retracement level from $70.02 to $61.20). A break above these levels could lead to $66.61 (the 200-day SMA). On the downside, a break below last week's low of $62.18 would target $61.00 (last week's low), with $60.78 (June 2 low) in the foreground. Stronger support lies at the psychologically important $60.00 level.

Consider going long on crude oil at $62.00 today. Stop-loss: $61.80, target: $63.50, $63.80.

Spot Gold

Gold prices surged to an all-time high of $3,749 per ounce on Monday, as investors await key US PCE inflation data and speeches from several Federal Reserve officials this week for further policy guidance. Last week, the Fed implemented its first interest rate cut of the year and hinted at further cuts to come amid a weakening labor market. Markets are currently pricing in another 25 basis point rate cut at the Fed's final two meetings of the year, in October and December. Expectations of continued monetary easing have significantly fueled gold's 40% surge so far this year. Gold is also supported by safe-haven demand due to ongoing geopolitical tensions and concerns about the economic impact of President Donald Trump's tariffs, coupled with aggressive central bank buying and continued ETF inflows.

Gold's performance is currently driven by both expectations of Fed policy and safe-haven demand. In the short term, if PCE inflation data slows this week, gold prices could re-approach or even break their all-time highs; however, if the data is stronger than expected, a market correction could be triggered. The daily chart shows that the moving average system maintains a bullish pattern, and the MACD indicator remains in positive momentum territory, but the momentum bar has narrowed, indicating a slowdown in the upward trend. Spot gold has found strong support near $3,674 (the 10-period simple moving average) on the 8-hour chart. Next levels to watch are $3,658 (the 34-period simple moving average) and $3.600 (the round-figure mark). Due to the new high of $3,715 set earlier this week, short-term resistance is concentrated at $3,750. A break above this level could push prices towards the all-time high of $3,800.

Consider going long on gold at 3,745 today, with a stop-loss at 3,740 and targets at 3,775 and 3,780.

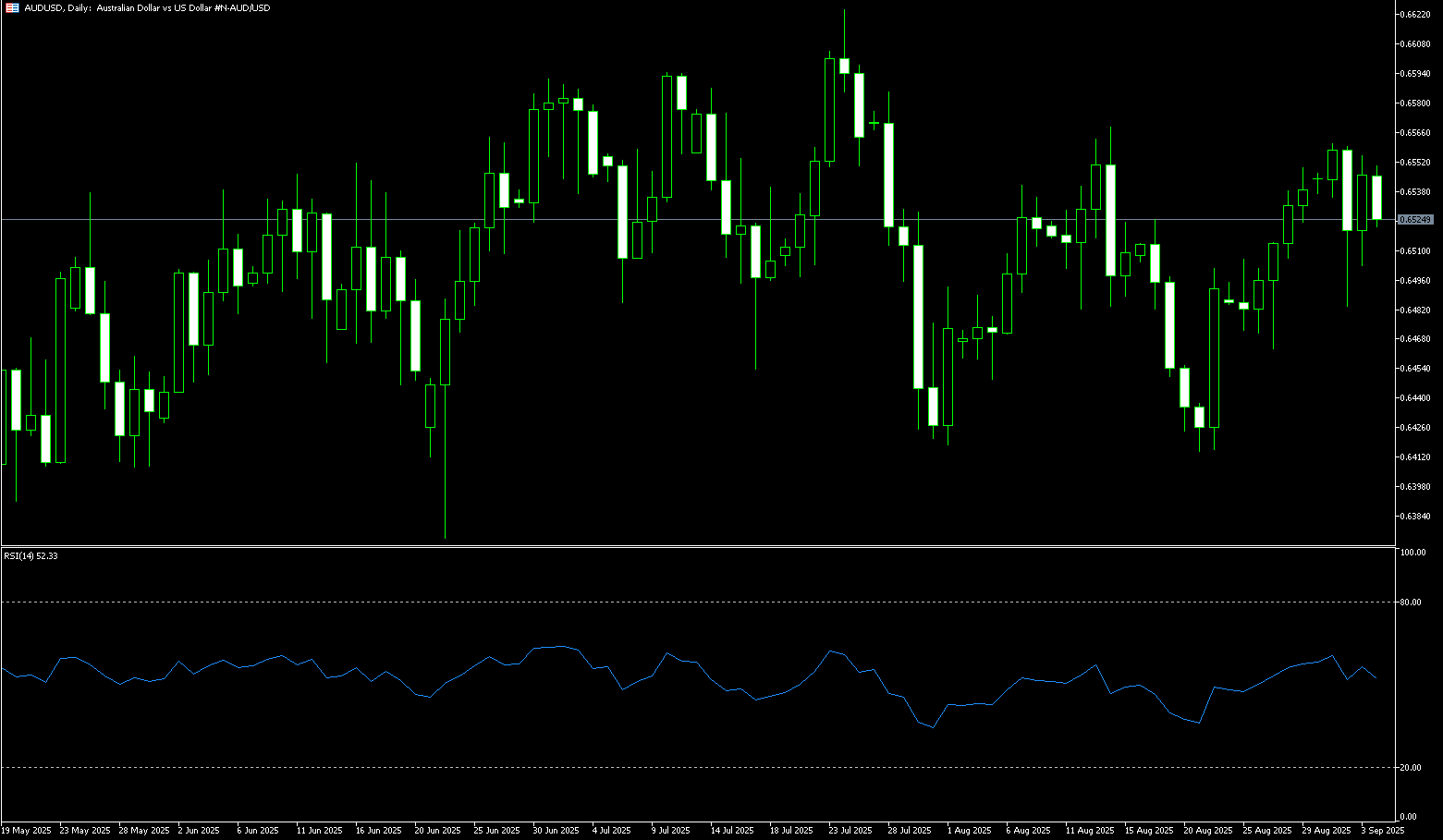

AUD/USD

The Australian dollar is under downward pressure as the Federal Reserve's less-than-expected dovish stance has revived the US dollar's upward momentum. AUD/USD has fallen for three consecutive trading days and fluctuated between 0.6590 and 0.6600 during Monday's Asian session. Risk reversals suggest growing bearish bets on the Australian dollar, while implied volatility continues to decline modestly. This week's focus will be on Australia's preliminary CPI and PMI data, as well as US PCE inflation data, which will determine whether the AUD/USD pair will continue its decline or find support. Price pressures remained elevated in July, but showed signs of easing. If August data continues this trend, it could boost market expectations for a slowdown in CPI data in Wednesday's monthly inflation report. However, last month's unexpectedly positive inflation rate raises questions about whether this is a temporary blip or the beginning of a new inflationary phase.

The US dollar's strong rebound cannot be ignored, having risen for four consecutive trading days since the Federal Reserve's interest rate meeting. At this point, the market volatility largely reflects short-covering after bets on a 50 basis point rate cut were dashed. The AUD/USD exchange rate's reversal near 0.6680 is unsurprising, as it forms a technical resonance between last week's high of 0.6706 and the round-figure mark of 0.6700. The key question now is how deep the pullback will be. Bears are likely targeting the 34-day simple moving average of 0.6546, with a break below that creating an initial target at the psychological level of 0.6500. On the other hand, the AUD/USD pair faces initial resistance at the key support level of 0.6636 (9-day simple moving average), but exceptionally strong inflation data may be needed to push the exchange rate above the round-figure mark of 0.6700 and last week's high of 0.6706.

Consider going long on the Australian dollar at 0.6590 today. Stop-loss: 0.6575. Target: 0.6640, 0.6650.

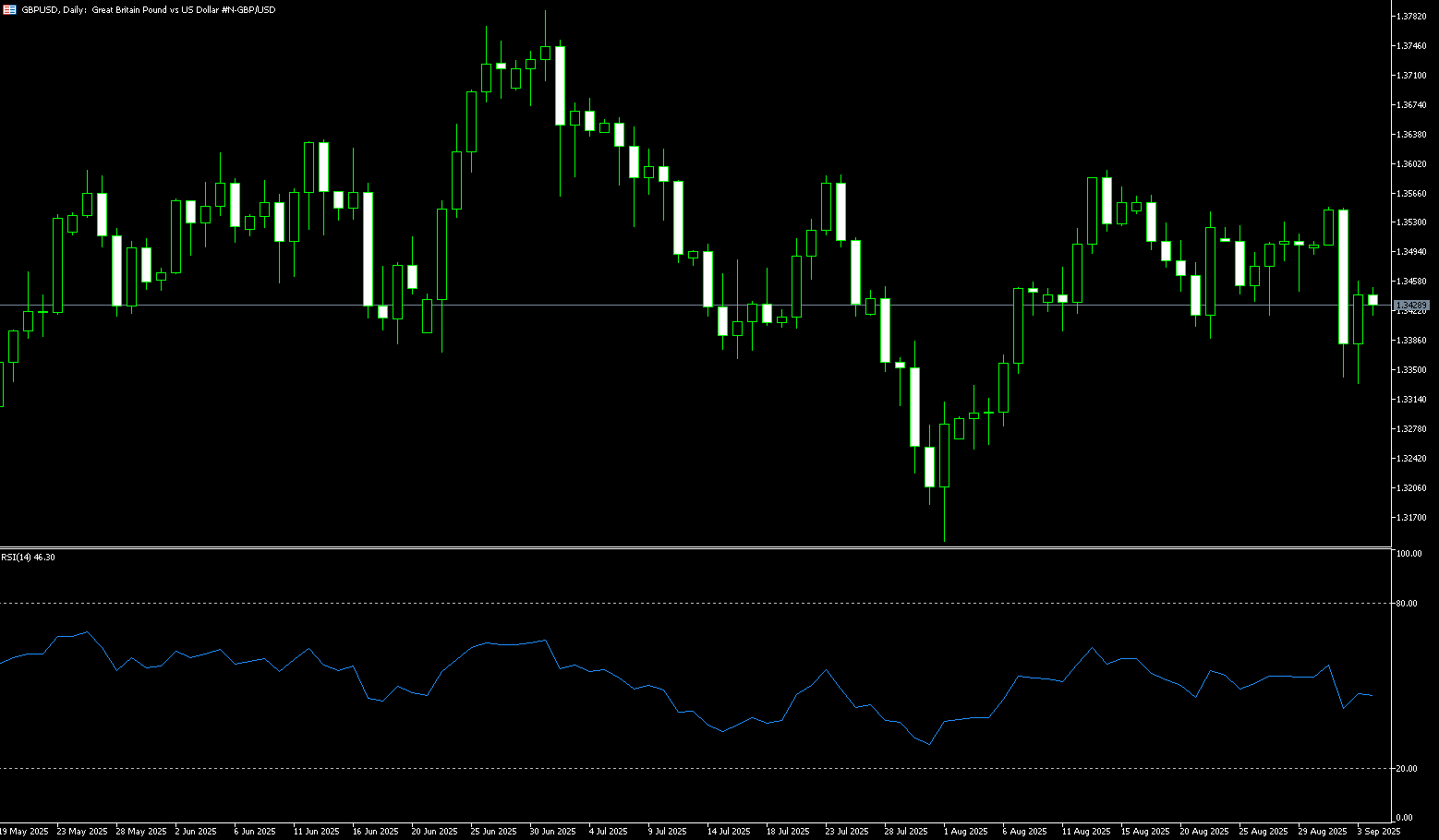

GBP/USD

GBP/USD recovered some ground during Monday's European session, rising just above 1.3500, snapping a three-day losing streak. However, potential upside for the pound may be limited given that UK Chancellor of the Exchequer Rachel Reeves may be unable to control the budget. Bank of England Chief Economist Hugh Peel is scheduled to speak. The latest public finance data showed public sector net borrowing reaching £18 billion, the highest level for the month in five years. Economists expected government borrowing to be significantly lower at £12.8 billion. Analysts believe this move could increase the debt burden and heighten fiscal risks, exerting some selling pressure on GBP/USD. The Bank of England voted on Thursday to keep interest rates at 4.0% due to uncertain growth prospects and a weak job market. This could help limit losses for the major currency pair in the short term.

GBP/USD continued its four-day downtrend, trading around 1.3500 in Asian trading on Monday. A bearish shift is emerging as technical analysis on the daily chart suggests the pair is poised to break below an ascending channel pattern. However, the 14-day relative strength index (RSI) remains below the 50 level, reinforcing the bearish bias. Furthermore, the pair is trading below its 20-day simple moving average at 1.3522, indicating weak short-term price momentum. GBP/USD is testing its key support level at the 1.3400 round number. A break below this channel would confirm the active bearish bias and exert downward pressure on the pair, potentially testing the monthly low of 1.3333 recorded on September 3. On the upside, GBP/USD could target near-term resistance at the 20-day simple moving average at 1.3522, followed by last Friday's high of 1.3560. A break above these levels would improve short- and medium-term price momentum and bring the pair closer to the psychologically important 1.3600 level.

Consider going long on the British pound at 1.3500 today. Stop-loss: 1.3486. Target: 1.3550, 1.3560.

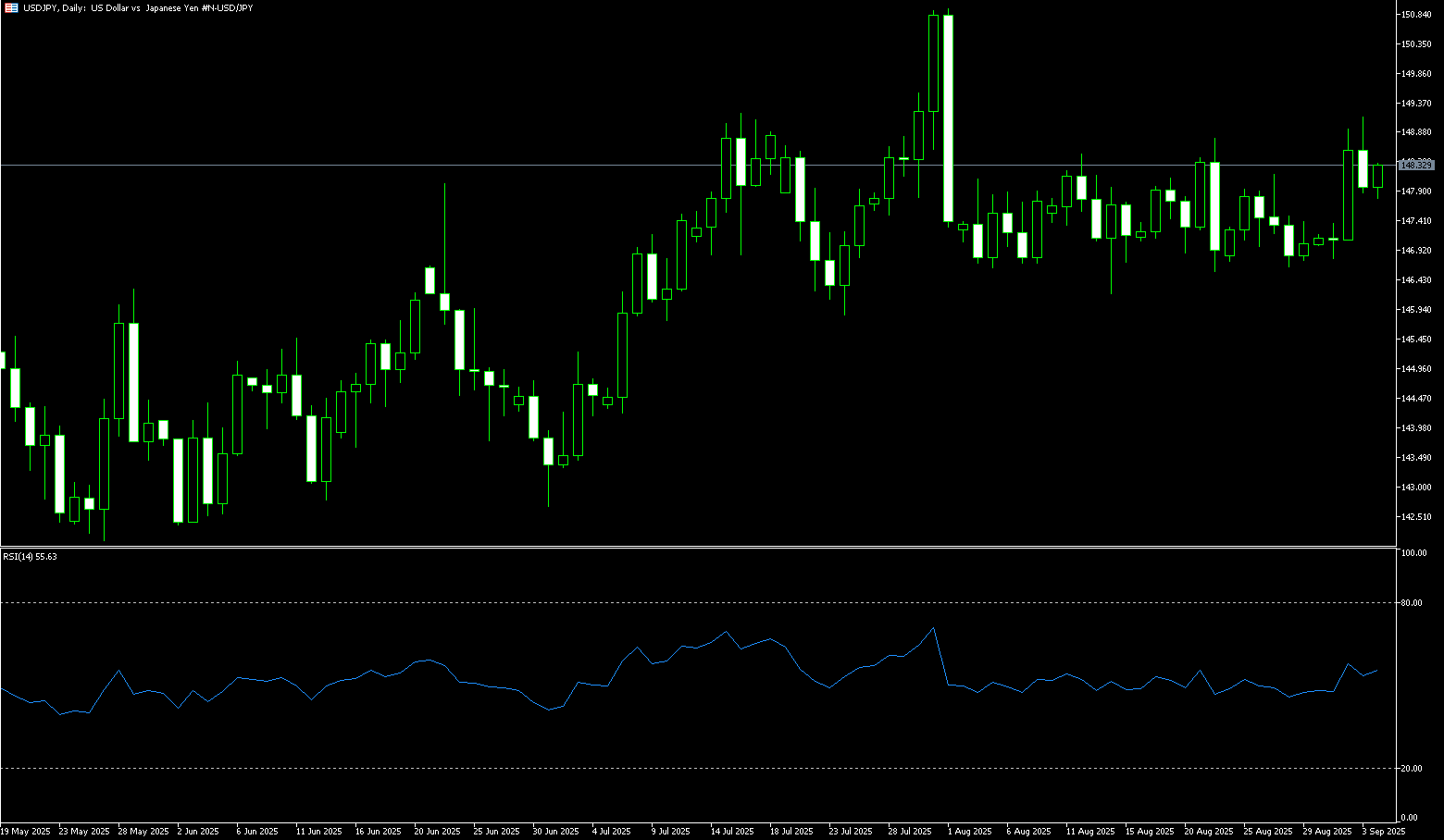

USD/JPY

The yen continued its downward trend on Monday, falling to around 148.00, extending its correction since hitting its highest point since July 7th last week. Market uncertainty over the timing and pace of the Bank of Japan's interest rate hikes meant the reaction to the hawkish decision to hold off was short-lived. Meanwhile, the positive sentiment in global risk assets weakened the yen's safe-haven appeal. Meanwhile, the Federal Reserve's policy tone contrasted sharply with that of the Bank of Japan. Last week, the Fed announced its first rate cut of the year and hinted at two more, citing a sluggish labor market and easing inflationary pressures. However, Powell emphasized after the meeting that the Fed was not in a rush to cut rates quickly, preferring a meeting-by-meeting approach. This cautious tone helped extend the dollar's rebound. Meanwhile, political uncertainty and economic pressures in Japan further weighed on the yen.

Overall, the trajectory of the dollar and yen hinges largely on the diverging policy paths of the Federal Reserve and the Bank of Japan. In the short term, the Federal Reserve's cautious stance is supporting the US dollar, while uncertainty surrounding the Bank of Japan's interest rate hikes is limiting the yen's potential for recovery. Looking at the daily chart, if USD/JPY stabilizes above 148.00, indicators will shift to positive territory, suggesting further upside potential. Above, resistance is concentrated around the 200-day simple moving average at 148.61. A break above this level could lead the exchange rate to test the 149.00 round number and the monthly high of 149.20. Conversely, support lies at 147.50 (the 9-day simple moving average). A break below this level could accelerate the decline towards 147.00, potentially even reaching 146.20 and 145.50, key lows since July 7.

Consider shorting the US dollar at 148.00 today. Stop-loss: 148.20, target: 147.00, 146.80.

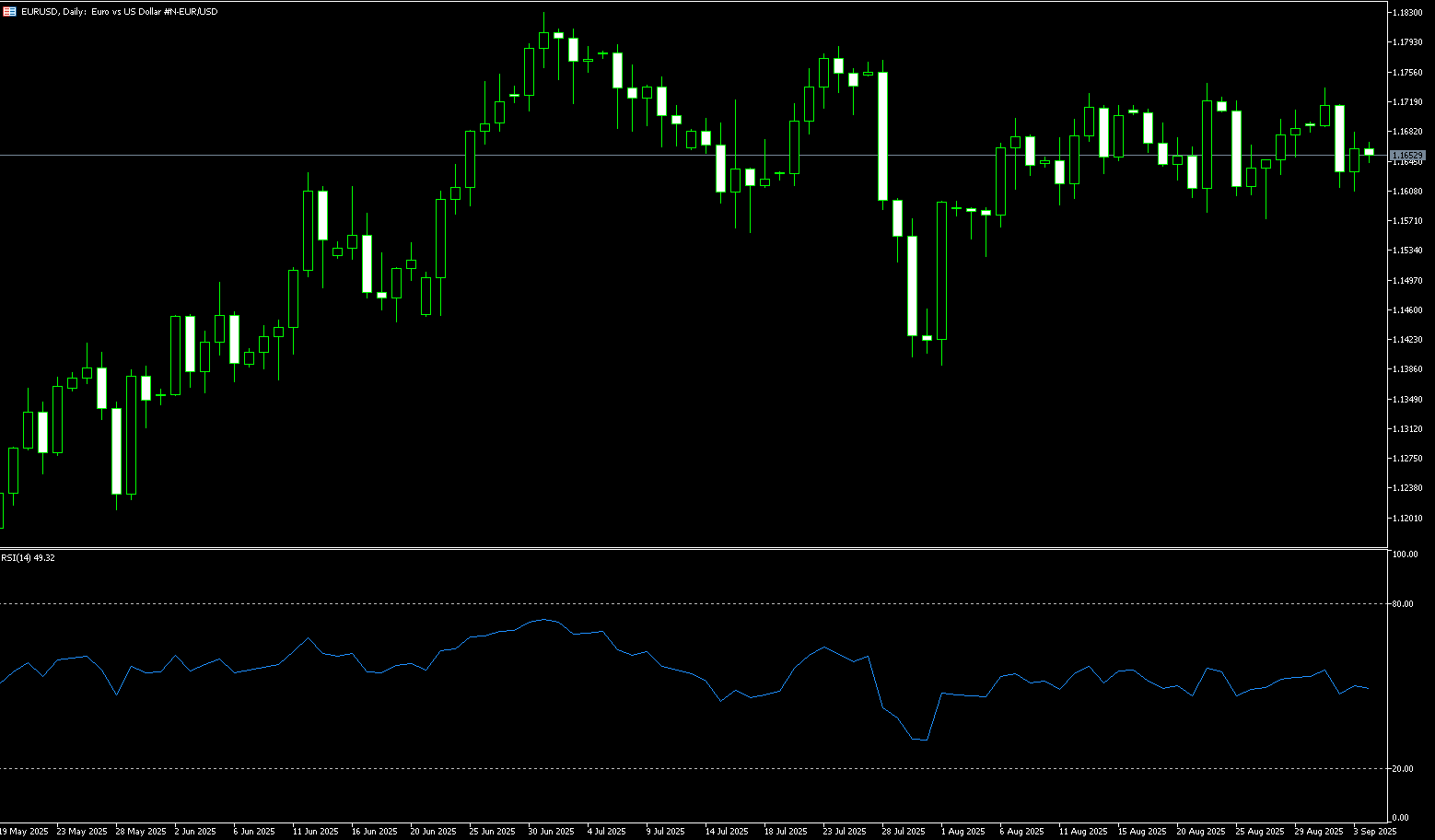

EUR/USD

During the European morning on Monday, EUR/USD rebounded to trade around 1.1790. Major currency pairs edged lower amid a rebound in the US dollar, as the Federal Reserve resumed its easing cycle last week. The Fed delivered its expected interest rate cut last week, but indicated it would not rush to reduce borrowing costs rapidly in the coming months. Fed Chairman Powell described the decision as a "risk-managed rate cut" aimed at addressing labor market slack while inflation remains relatively high. Powell's comments suggested a less dovish stance than some investors had anticipated. This, in turn, provided some support for the US dollar and created resistance for major currency pairs. Traders will closely monitor their views on the economy and central bank independence. Concerns about the Fed's independence may limit the dollar's upside in the short term.

EUR/USD retreated after recent gains, forming an "evening star" pattern, confirming the euro's weakness. While bears have yet to break through the September 11 low of 1.1660, they are gathering some momentum. A break above the 1.1700 level would expose the latter, as well as the confluence of the 100-day simple moving average and the August 27 swing lows near 1.1567 and 1.1574. The 14-day relative strength index (RSI) on the daily chart continues to support the broader uptrend, remaining just outside overbought territory. A break above 1.1800 would open the door to 1.1850 and potentially a retest of the year-to-date high of 1.1919.

Consider a long position on the euro at 1.1785 today, with a stop loss at 1.1740 and a target at 1.1840 or 1.1850.

Disclaimer: The information contained herein (1) is proprietary to BCR and/or its content providers; (2) may not be copied or distributed; (3) is not warranted to be accurate, complete or timely; and, (4) does not constitute advice or a recommendation by BCR or its content providers in respect of the investment in financial instruments. Neither BCR or its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

更多报道

风险披露:衍生品在场外交易,采用保证金交易,意味着具有高风险水平,有可能会损失所有投资。这些产品并不适合所有投资者。在进行交易之前,请确保您充分了解风险,并仔细考虑您的财务状况和交易经验。如有必要,请在与BCR开设账户之前咨询独立的财务顾问。

BCR Co Pty Ltd(公司编号1975046)是一家根据英属维尔京群岛法律注册成立的公司,注册地址为英属维尔京群岛托尔托拉岛罗德镇Wickham’s Cay 1的Trident Chambers,并受英属维尔京群岛金融服务委员会监管,牌照号为SIBA/L/19/1122。

Open Bridge Limited(公司编号16701394)是一家根据2006年《公司法》注册成立并在英格兰和威尔士注册的公司,注册地址为 Kemp House, 160 City Road, London, City Road, London, England, EC1V 2NX.本公司仅作为支付处理方运作,不提供任何交易或投资服务。

English

English

简体中文

简体中文

繁體中文

繁體中文

Bahasa

Melayu

Bahasa

Melayu

Tiếng

Việt

Tiếng

Việt

ไทย

ไทย

日本語

日本語

한국어

한국어

ភាសាខ្មែរ

ភាសាខ្មែរ

español

español